THE YEAR-END FINANCIAL STATEMENT PROCESS:

A Practical Guide for Small Nonprofit Organizations having a CPA Audit (or Review)

(Part 2 of 5)

Part II: DIFFERENT ROLES IN THE AUDIT PROCESS

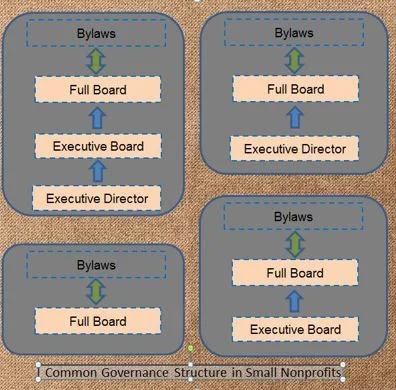

A. Governance’s Role in the Audit Process (The Board):

Unlike a small business, a nonprofit organization does not have “owners”. A nonprofit is “governed” by a board of directors under the direction of the organization’s bylaws and state law. The Attorney General (or other state official) provides oversight and regulates all the charities operating in the state. Additionally, because of its tax exempt status, the organization must adhere to IRS regulations as well. The board acts as trustee of the organization's assets and ensures that the nonprofit is well managed, fiscally sound and adhering to its mission and exempt purpose. In doing so, the board must exercise proper oversight of the organization's operations and maintain the legal and ethical accountability of its staff and volunteers. Generally, board members are legally responsible and have the ultimate authority over the organization. All board members should be familiar with the organization’s bylaws, finances, annual audit and Form 990. The executive director may manage the day to day operations, but major decisions should have direct board approval. It is also important that matters involving the executive director’s compensation be decided by the board. All audits will involve governance (the board). In the absence of an audit committee, the independent board members (i.e., unpaid) will perform the audit oversight function. This involves the following basic duties: (1) Overseeing the accounting and financial reporting processes of the organization and the audit of its financial statements; (2) Annually retaining or renewing the retention of an independent auditor; and (3) Reviewing with the independent auditor the results of the audit (including the management letter). All board matters should be documented in proper meeting minutes. The organization is required to have a Conflict of Interest policy to show how it makes decisions involving interested (i.e., related) parties.

B. Management’s Role in the audit process: (Executive Director)

In many organizations, the board hires an executive director to manage the operations. The position usually reports to the executive committee or directly to the full board of directors. In most cases, a paid executive director is not a voting member of the board but the bylaws of an organization may dictate otherwise. Although not on the audit committee, the executive director will usually be the point person and work with the auditor during the audit process.

C. The Independent Accountant’s Role in the Audit Process (CPA)

In a financial statement audit, the CPA expects the organization’s management to present the financial statement figures at year end. Furthermore the auditors will want explanations and evidence to support the figures.

Audits and Reviews are attest engagements that require independence. Services performed in conjunction with Audits or Reviews are called non-attest services. Specific rules have to be followed regarding non-attest services in order for the CPA to remain independent. Some non-attest services that frequently are performed in conjunction with an audit (or review) engagement are financial statement preparation, accounting adjustments, reconciliations, functional expense allocation assistance and tax preparation. Original bookkeeping or major overhauls of financial data cannot be performed in an attest engagement. Importantly, the auditor cannot participate in the decision making process of the client. Audit standards also dictate that if the auditor assists too significantly in the financial statement preparation process, independence could be deemed to be impaired. In order to remain independent while performing these non-attest services, special precautions have to be followed. The organization’s management has to be responsible for the non-attest service by doing the following (1) designating an individual who possesses suitable skills to oversee the service; (2) evaluate the adequacy and results of the services performed; and (3) accept responsibility for the results. Under no circumstances can the CPA assume management responsibilities in an attest engagement. Some organizations hire an accountant or qualified bookkeeper to perform year-end close services before an audit or review engagement begins.

Auditing standards also require certain “disclosures” to be made by the organization. These come in the form of footnotes that follow the financial statements. The CPA’s assistance in preparing the footnotes disclosures is another type of non-attest service. The auditor will need to obtain information and evidence to support the financial statement disclosures. Common areas requiring disclosures are Accounting Policies, Fixed Assets, Notes Payable, Leases, Related Parties, Contingencies, Retirement Plans, Restricted Net Assets, Pledges / Contributions, Joint Costs and Subsequent Events.

The following language is part of the standard engagement letter which outlines the auditor’s role:

Audit procedures will include tests of documentary evidence supporting the transactions recorded in the accounts, tests of the physical existence of assets, and direct confirmation of receivables and certain assets and liabilities by correspondence with selected individuals, funding sources, creditors, and financial institutions…. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements….An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements…..Our audit will include obtaining an understanding of the Organization and its environment, including internal control, sufficient to assess the risks of material misstatement of the financial statements and to design the nature, timing, and extent of further audit procedures.